In this article we will discuss eleven high growth application software stocks to invest in now.

If you’ve been watching the markets lately, one thing’s becoming crystal clear, software stocks are making a strong comeback. After a tough stretch of macro headwinds, rising interest rates, and cautious enterprise spending, 2025 is shaping up to be a turning point. Whether you are a retail investor looking to ride the AI wave or a long term portfolio builder focused on scalable business models, the application software space offers some seriously compelling opportunities right now.

So what’s driving the momentum for Application Software Stocks?

According to Morgan Stanley, enterprise software budgets are stabilizing, and more importantly, front office software spending is heating up. Their Q2 2025 CIO survey shows that 52% of CIOs plan to increase spending on front office SaaS that includes CRM, marketing tools, and customer service platforms, compared to just 7% planning cuts. That’s a hefty 7.5x up to down ratio, indicating real confidence in this segment. On average, CIOs expect front office SaaS spending to grow 4.7% year over year, outpacing back office software for the first time in years. That’s a big shift, and it tells us where enterprise dollars are heading.

Another major catalyst? Generative AI. It’s no longer just a buzzword. Businesses are starting to deploy Gen AI tools into core functions like sales, support, and analytics. As a result, application software companies, especially those with AI native platforms, are seeing renewed interest from investors and customers alike.

Let’s not forget the broader economic picture either. While Morgan Stanley’s report shows some expected softening in U.S. consumer spending this year, businesses are still investing in efficiency enhancing technologies. And that’s where modern software solutions shine, cutting costs, improving performance, and enabling smarter decision making.

So where should investors look? In this article, we’ve handpicked 11 high growth application software stocks that are not just riding the AI and digital transformation trends, they are helping lead them. From cloud native CRMs to cutting edge analytics platforms, these companies offer a mix of solid fundamentals, high growth potential, and strong market demand.

If you’re looking to diversify your portfolio with quality software stocks, now’s a great time to dig deeper. The future of work is digital, and these companies are building the tools that power it. Let's dive in.

Our methodology for selecting the best high growth application software stocks

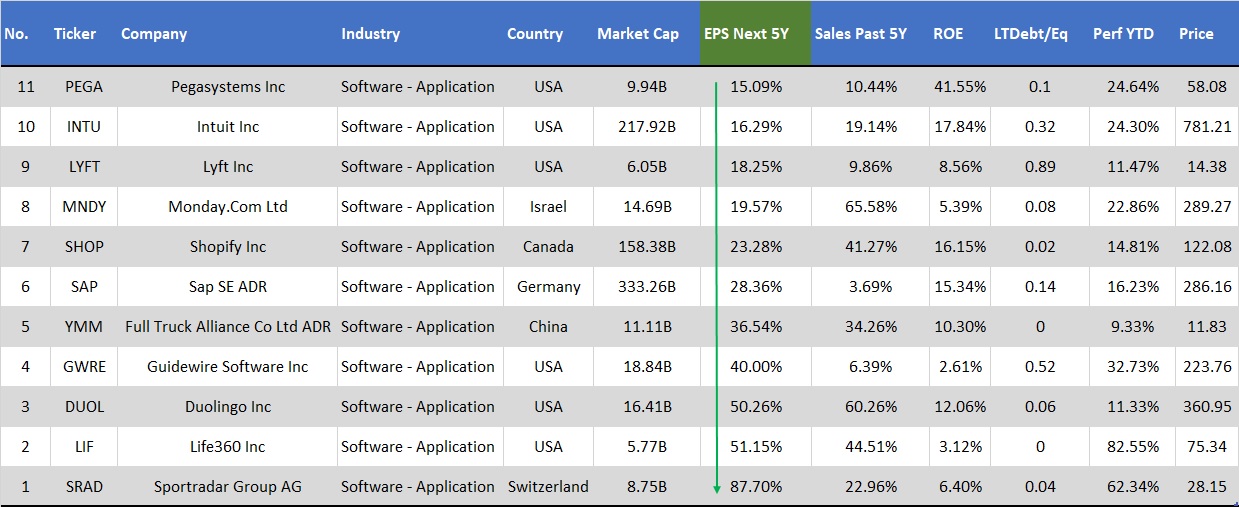

To compile this list of the eleven high growth application software stocks to invest in now, we used data from the Finviz stock screener. We applied a set of criteria designed to identify fundamentally strong, actively traded companies with positive investor sentiment. Specifically, we filtered for mid cap and large cap companies with an average daily trading volume above 500,000 shares and a stock price above $10. Additionally, we only included stocks that have received a "Buy" or better consensus rating from Wall Street analysts and have posted a positive year to date (YTD) performance. All selected companies have strong earnings growth projections, as indicated by their estimated EPS growth over the next five years. The stocks are arranged in ascending order based on their projected EPS growth figures.

11 High Growth Application Software Stocks To Invest In Now

11. Pegasystems Inc. (NASDAQ:PEGA)

Projected EPS growth for the next five years: 15.09%

Pegasystems Inc. (NASDAQ:PEGA) is a global enterprise software company known for its AI powered automation tools. Its main platform, Pega Infinity, helps businesses streamline operations, improve customer service, and automate decision making across industries like banking, insurance, healthcare, and telecom.

In Q2 2025, Pegasystems Inc. (NASDAQ:PEGA) beat expectations on all key metrics, revenue, EPS, free cash flow, total ACV, and cloud ACV. Annual contract value (ACV), a key performance indicator, grew 16% year over year, while cloud ACV jumped 28%, reflecting strong demand for its SaaS offerings. Free cash flow reached $286 million, with a large portion used for share buybacks, showing confidence in long term performance.

A major growth driver is Pega GenAI Blueprint, a low code, AI powered development tool that allows users to modernize legacy systems quickly. Over 1,000 companies are already building applications using Blueprint, including global partners like Accenture and Infosys, which are creating their own customized versions to serve enterprise clients.

The company also signed a 5 year strategic partnership with AWS, enhancing its cloud reach and offering joint solutions for legacy system transformation. The collaboration includes integrating Pega Blueprint with AWS Transform, enabling clients to modernize legacy systems faster without disrupting core operations. This move improves access to Pegasystems Inc. (NASDAQ:PEGA) software via the AWS Marketplace and positions the company to win larger enterprise cloud deals.

On July 24, RBC Capital analyst Rishi Jaluria raised the price target for Pegasystems Inc. (NASDAQ:PEGA) from $60 to $70 while keeping an Outperform rating. The upgrade comes after the company delivered strong results in Q2, beating expectations across key metrics including Total ACV, Cloud ACV, revenue, EPS, and free cash flow. RBC believes Pegasystems offers an attractive risk/reward opportunity for investors.

10. Intuit Inc. (NASDAQ:INTU)

Projected EPS growth for the next five years: 16.29%

Intuit Inc. is a leading U.S. based application software company known for solutions like TurboTax, QuickBooks, Credit Karma, and Mailchimp. Intuit Inc. (NASDAQ:INTU) remains one of the strongest application software stocks in 2025. In Q3 FY2025, Intuit Inc. (NASDAQ:INTU) delivered revenue of $7.8 billion (up 15% YoY) and beat earnings expectations with non GAAP EPS of $11.65 versus the expected $10.93. The company’s AI powered platform strategy is driving performance across both consumer and business segments, with innovations that improve automation, personalization, and time to value for customers.

TurboTax Live saw 24% user growth and 47% revenue growth, fueled by AI enabled features that cut tax prep time and improved customer conversion. QuickBooks Online revenue rose 21%, supported by higher pricing and strong user adoption. Business platform revenue grew 19%, with online ecosystem revenue up 20%, highlighting the increasing relevance of Intuit's tools for small and mid market businesses.

Intuit Inc. (NASDAQ:INTU) is also expanding its presence in the mid market with Intuit Enterprise Suite (IES), which saw a 40% increase in online ecosystem revenue. AI generated invoice reminders boosted overdue payment rates, while new features like multi entity expense management and dimensional P&Ls enhanced platform utility.

From analysts standpoint, on July 28, Oppenheimer analyst Scott Schneeberger raised the price target for Intuit Inc. (NASDAQ:INTU) from $742 to $868, while reaffirming an Outperform rating. The revised target reflects continued confidence in the company’s outlook, with no change to the previous bullish stance.

09. Lyft, Inc. (NASDAQ:LYFT)

Projected EPS growth for the next five years: 18.25%

Lyft, Inc. (NASDAQ:LYFT), best known for its ride hailing platform, is rapidly evolving into a broader software driven mobility company. In 2025, Lyft, Inc. (NASDAQ:LYFT) continues to demonstrate strong growth fundamentals, driven by innovation in pricing, customer experience, and international expansion, key indicators for investors looking at high growth software stocks.

The company posted record levels in gross bookings, adjusted EBITDA, and free cash flow. This marked the 16th consecutive quarter of double digit year over year growth in gross bookings, underlining consistent demand and effective execution. Lyft also expanded its share repurchase program to $750 million, signaling confidence in its financial health.

Notably, Lyft, Inc. (NASDAQ:LYFT) is investing in new demographics through Lyft Silver, targeting older riders, and expanding geographically through its acquisition of FREENOW, a European mobility platform operating in nine countries. Growth in Canada has also been strong, with driver onboarding now open in Quebec.

On the product side, Lyft, Inc. (NASDAQ:LYFT) is enhancing rider reliability with features like Price Lock and driver feedback tools like the Smooth Cruiser score. Its partnerships in autonomous vehicles (AVs) and fleet management (e.g., Flexdrive and Marubeni) suggest a long term strategy to diversify and optimize ride supply using AI powered platforms.

On July 21, Sanford C. Bernstein raised its price target for Lyft (NASDAQ: LYFT) from $16 to $18, maintaining a market perform rating. Analyst Nikhil Devnani expects Q2 results to meet or slightly exceed guidance, projecting 13% year over year growth in gross bookings and $125 million in adjusted EBITDA. The firm noted that Q1 benefited from lower general and administrative expenses, which are unlikely to repeat. Bernstein emphasized that Lyft doesn’t need to beat expectations to gain investor trust, solid, consistent results could help improve its valuation. They also anticipate updates on Lyft’s May Mobility partnership, though they remain cautious on its near term impact.

08. monday.com Ltd. (NASDAQ:MNDY)

Projected EPS growth for the next five years: 19.57%

monday.com Ltd. (NASDAQ:MNDY) is a fast growing software company that helps teams manage projects, workflows, and daily tasks with ease and flexibility. As one of the standout names among application software stocks, it continues to show strong business performance and product innovation that should interest both short term and long term investors.

In Q1 2025, monday.com Ltd. (NASDAQ:MNDY) grew revenue by 30% year over year and posted record operating profit and cash flow. The company holds $1.53 billion in cash, backed by strong free cash flow and a solid 90% gross margin, proof of its efficient, scalable model.

The company is expanding quickly in the enterprise space, thanks to its growing suite of AI powered tools across CRM, Dev, and Service products. Today, 70% of monday Service’s revenue comes from mid market and enterprise clients. AI usage on the platform rose 150% in one quarter, showing fast adoption by customers.

On June 17, monday.com (NASDAQ: MNDY) announced the appointment of Harris Beber as Chief Marketing Officer, effective July 3. Beber previously led marketing at Google Workspace, Waze, Vimeo, and held senior roles at Amazon and Shutterfly. monday.com Ltd. (NASDAQ:MNDY) also brought in a new Chief Revenue Officer with a strong background in enterprise software to drive global growth.

On June 17, Morgan Stanley began coverage on monday.com Ltd. (NASDAQ:MNDY) with an Equal weight rating. The firm highlighted the company’s move toward larger enterprise clients and a multi product strategy as a major growth opportunity, though it noted execution risks. monday.com recently crossed $1 billion in annual recurring revenue and is now shifting to a more sales led model. Morgan Stanley also mentioned potential future acquisitions, a change from its past organic growth approach. While the company has outperformed peers, the firm believes its current valuation already prices in much of the upside.

07. Shopify Inc. (NASDAQ:SHOP)

Projected EPS growth for the next five years: 23.28%

Shopify Inc. (NASDAQ:SHOP) remains one of the most agile and globally scalable software stocks in the e commerce space. Despite narrowly missing Q1 2025 EPS estimates by a cent, the company posted 27% year over year revenue growth and a 15% free cash flow margin, highlighting its operational efficiency and strong unit economics.

Shopify Inc. (NASDAQ:SHOP) platform powers over 1 million businesses globally, with continued momentum across both small merchants and large enterprises. The company’s GMV (Gross Merchandise Volume) has now grown over 20% for seven straight quarters, driven by strength in B2B, offline, and international segments. European GMV grew 36% YoY, while offline GMV rose 23%, confirming Shopify’s omnichannel reach.

The firm is investing in key infrastructure like AI driven tools e.g., TariffGuide.ai and Sidekick, new payment capabilities in 39 countries, and cross border trade simplification, all critical for modern commerce. Shopify Payments hit 64% GMV penetration in Q1. New large brand wins e.g., VF Corp, FAO Schwartz, and Caring Beauty further prove Shopify Inc. (NASDAQ:SHOP) appeal to enterprise clients.

On July 28, Scotiabank raised its price target for Shopify Inc. (NASDAQ:SHOP) from $90 to $115 while maintaining a Sector Perform rating, reflecting growing optimism around the company’s near term prospects. The upgrade is largely driven by continued strength in the U.S. e-commerce sector, where Shopify Inc. (NASDAQ:SHOP) remains a key platform for both small and large merchants. The firm also pointed to Shopify’s expanding footprint in international markets and its increasing penetration among enterprise level clients as major growth drivers. These developments, coupled with expectations for a potential beat in gross merchandise volume (GMV) and overall revenue in the coming quarters, support the higher valuation.

06. SAP SE (NYSE:SAP)

Projected EPS growth for the next five years: 28.36%

SAP SE (NYSE:SAP) is a global leader in enterprise application software and continues to position itself as a top tier software stock for growth focused investors. In Q2 2025, SAP delivered strong performance across key metrics: cloud revenue rose 28% year over year, driven by continued demand for its Cloud ERP Suite, which has now grown at 30%+ for 14 consecutive quarters. Operating profit surged 35%, reflecting the success of its ongoing transformation and disciplined cost control.

SAP SE (NYSE:SAP) cloud backlog climbed to €18.1 billion, underscoring robust future demand, even in the face of macro uncertainties like tariffs and elongated sales cycles in public sector and industrial clients. Strategic wins this quarter included partnerships with Alibaba, Adobe, and BMW, along with growing enterprise adoption of AI and data tools across finance, HR, and supply chain.

AI is central to SAP SE (NYSE:SAP) long term growth. Over half of SAP’s Q2 cloud order volume included AI use cases, and the company plans to launch 40 AI agents by year end to boost automation across business functions. The launch of Business Data Cloud and Joule AI assistant further enhance SAP’s competitive moat.

On July 24, Barclays raised its price target for SAP SE (NYSE:SAP) from $308 to $322 while reiterating its Overweight rating, citing strong cloud performance. The firm noted SAP SE (NYSE:SAP) cloud revenue growth is trending toward the high end of its 26–28% guidance, while current cloud backlog rose 28%, in line with expectations. Despite macro uncertainties, including delays in U.S. public sector and manufacturing decisions, Barclays sees Q3 cloud revenue staying strong before moderating in Q4, keeping SAP SE (NYSE:SAP) on track for its full year targets. SAP SE (NYSE:SAP) maintains a solid 73.8% gross margin and 10.3% annual revenue growth.

05. Full Truck Alliance Co. Ltd. (NYSE:YMM)

Projected EPS growth for the next five years: 36.54%

Full Truck Alliance Co. Ltd. (NYSE:YMM) is a leading digital freight platform in China that connects millions of shippers and truckers through advanced logistics software. As the country’s logistics sector continues to digitize, Full Truck Alliance Co. Ltd. (NYSE:YMM) is strategically placed to dominate this shift by replacing inefficient offline models with intelligent, tech driven freight matching.

Looking ahead, Full Truck Alliance Co. Ltd. (NYSE:YMM) plans to deepen investments in artificial intelligence and autonomous trucking through its expanded stake in Plus PRC. This move positions FTA at the forefront of automating heavy duty logistics, a major future growth driver. With nearly 30 million small and medium sized shippers still underserved, the company is aggressively targeting this untapped segment through nationwide brand initiatives and product enhancements.

To boost platform quality and retention, Full Truck Alliance Co. Ltd. (NYSE:YMM) is refining its matching algorithm, enhancing trucker tools, and personalizing pricing structures for shippers. These steps are designed to improve order conversion, lower logistics costs, and drive long term user loyalty. The company also plans to implement dynamic pricing, intelligent risk controls, and AI powered matching systems to further improve efficiency and monetization.

On May 22, Citi lowered its price target for Full Truck Alliance Co. Ltd. (NYSE:YMM) from $16.50 to $16.00 but maintained a Buy rating on the stock. The modest revision followed the company’s solid quarterly performance, which included strong order volume growth and an earnings beat. While short term investments may affect margins, Citi underscored Full Truck Alliance Co. Ltd. (NYSE:YMM) strong fundamentals and long term growth prospects. The firm remains optimistic about continued order volume growth and views the company as well positioned in China's evolving digital freight and logistics sector.

04. Guidewire Software, Inc. (NYSE:GWRE)

Projected EPS growth for the next five years: 40.00%

Guidewire Software, Inc. (NYSE:GWRE) is a leading application software company that provides cloud based core systems for property and casualty (P&C) insurers. Its solutions help insurers modernize operations, launch new products faster, and improve customer service through a unified, data driven platform.

The company is emerging as a key player in the digital transformation of the insurance industry. Its flagship Guidewire Cloud Platform continues to gain traction globally, with 17 new cloud deals closed in Q3 FY2025, including seven with Tier 1 insurers, driving annual recurring revenue (ARR) to $960 million. Management expects to cross the $1 billion ARR milestone this year, supported by strong customer retention, product expansion, and international growth.

Recent wins across North America, Europe, APAC, and Latin America reflect the platform’s flexibility and scalability. Guidewire’s InsuranceSuite and InsuranceNow products are gaining ground, appealing to both large and mid sized insurers looking to replace legacy systems with agile solutions.

With strategic investments in AI, pricing tools (through its acquisition of Quanti), and local market development (notably in Japan and Europe), Guidewire Software, Inc. (NYSE:GWRE) is expanding its innovation lead. The firm’s strong balance sheet, growing customer base, and deep partner network further support long term upside.

On July 21, Baird raised its price target on Guidewire Software, Inc. (NYSE:GWRE) from $265 to $270, maintaining an Outperform rating. The firm cited strong momentum in the P&C insurance market, growing cloud adoption, and record Q3 sales as key drivers. Baird sees continued growth in ARR and reaffirmed Guidewire Software, Inc. (NYSE:GWRE) leading position in insurance software.

03. Duolingo, Inc. (NASDAQ:DUOL)

Projected EPS growth for the next five years: 50.26%

Duolingo, Inc. (NASDAQ:DUOL) is a leading mobile first language learning platform and one of the fastest growing software stocks in the edtech sector. With over 130 million active users globally and consistent double digit DAU growth, the company continues to expand its reach across both emerging and mature markets.

Investors may find Duolingo’s product led growth strategy particularly appealing. Its monetization model relies on ad supported users and paid subscriptions (Super and Max tiers), the latter now making up a growing share of revenue. Notably, Duolingo Max, its premium AI powered offering, now accounts for 7% of total subscribers, with even higher uptake among English learners.

The company’s investment in generative AI is significantly enhancing its product development speed and efficiency. With AI generated course content, Duolingo added 148 new language modules in one year, a tenfold acceleration compared to its past pace.

Beyond language, the company is diversifying into math, music, and even chess, creating new engagement and monetization opportunities. Its ability to scale features built by non engineers using AI is a long term advantage.

Citizens JMP lowered its price target on Duolingo, Inc. (NASDAQ:DUOL) from $475 to $450, citing a slowdown in user engagement based on third party data. Despite the adjustment, the firm maintained its "Outperform" rating, reflecting continued confidence in Duolingo, Inc. (NASDAQ:DUOL) long term growth. The downgrade follows Sensor Tower data showing a decline in daily active user (DAU) growth, from 51% in Q1 to around 39% in Q2. This trend also prompted JPMorgan to cut its target recently. While near term engagement appears to be cooling, Citizens JMP still sees Duolingo, Inc. (NASDAQ:DUOL) AI driven platform and global reach as strong long term assets, viewing the dip as a buying opportunity for investors.

02. Life360, Inc. (NASDAQ:LIF)

Projected EPS growth for the next five years: 51.15%

Life360, Inc. (NASDAQ:LIF) is a fast growing software stock known for its mobile first platform that provides real time location sharing, safety alerts, and tracking solutions for families, pets, and valuables. The company operates on a freemium model and earns revenue primarily from subscriptions and recurring services.

Life360, Inc. (NASDAQ:LIF) is demonstrating strong long term growth potential, with projected earnings per share (EPS) growth of 51.15% over the next five years and an impressive five year historical sales growth rate of 44.51%, highlighting the company’s ability to scale revenue and expand profitability over time.

In Q1 2025, Life360, Inc. (NASDAQ:LIF) reported a 26% year over year increase in paying circles, reaching 2.4 million, and 39% growth in international monthly active users. These strong metrics contributed to a 32% YoY revenue growth, supported by a successful premium pricing strategy and robust subscriber retention. The company also achieved a 39% increase in average revenue per paying user internationally.

Partnerships with Aura and AccuWeather are expanding monetization opportunities. Aura adds enterprise exposure via a B2B2C channel, while AccuWeather enhances user value with real time severe weather alerts. Life360 is also preparing to launch a pet tracker, integrated within its app, to further grow subscription revenue.

On May 12, Canaccord raised its price target on Life360, Inc. (NASDAQ:LIF) from $75 to $86, reiterating a Buy rating. Despite a 13% decline in hardware revenue and near term tariff risks, Life360, Inc. (NASDAQ:LIF) rapid user growth, expanding ecosystem, and global reach make it a standout in the high growth application software space.

01. Sportradar Group AG (NASDAQ:SRAD)

Projected EPS growth for the next five years: 87.70%

Sportradar Group AG (NASDAQ:SRAD) is a Switzerland based software stock operating at the intersection of real time sports data, betting technology, and media services. The company delivered record quarterly revenue of €311 million in Q1 2025, a 17% year over year increase, driven by rising global demand for its betting and sports content solutions. U.S. revenue grew 31%, now accounting for 28% of total sales, supported by exclusive rights with leagues like the NBA, NHL, and MLB.

Sportradar Group AG (NASDAQ:SRAD) core value lies in its deep data infrastructure and AI powered product suite, which fuels real time odds, live betting markets, and immersive fan engagement tools. Key innovations, such as 4Sight streaming, Alpha Odds, and emBET, are enabling sportsbook clients to deliver personalized in play betting experiences at scale. With only 40% of clients using 4 or more Sportradar products, there is significant headroom for wallet share expansion.

The company’s recent acquisition of IMG Arena’s rights portfolio at no net cost enhances its long term content moat, while its €2 billion in contracted revenue provides strong cash flow visibility.

On July 21, Goldman Sachs initiated coverage on Sportradar Group AG (NASDAQ:SRAD) with a Neutral rating and a $31 price target. The firm cited strong revenue growth from online sports betting and increased product adoption. Sportradar has returned 170% over the past year, with 23% revenue growth and $415 million EBITDA in the last 12 months. Multi year deals with major sports leagues provide visibility into costs and earnings. Goldman expects 30% EBITDA and free cash flow growth through 2027 but sees the stock as fully valued, trading at a 40% premium to peers after a 75% YTD rally.

Read Next:

- 10 Best Performing US Stocks in 2025 So Far

- 10 Best Uranium Stocks to Buy in 2025 as Nuclear Energy Demand Rises

- 7 High Dividend Tech Stocks to Buy for Long Term Growth in 2025

Disclaimer: This article is for informational purposes only. See our full disclaimer. The article is originally published on TheRichStocks.com.

(1)")